GridTrader.xyz

"An investment operation is one which, upon thorough analysis, promises safety of principal and an adequate return. Operations not meeting these requirements are speculative. - Benjamin Graham"

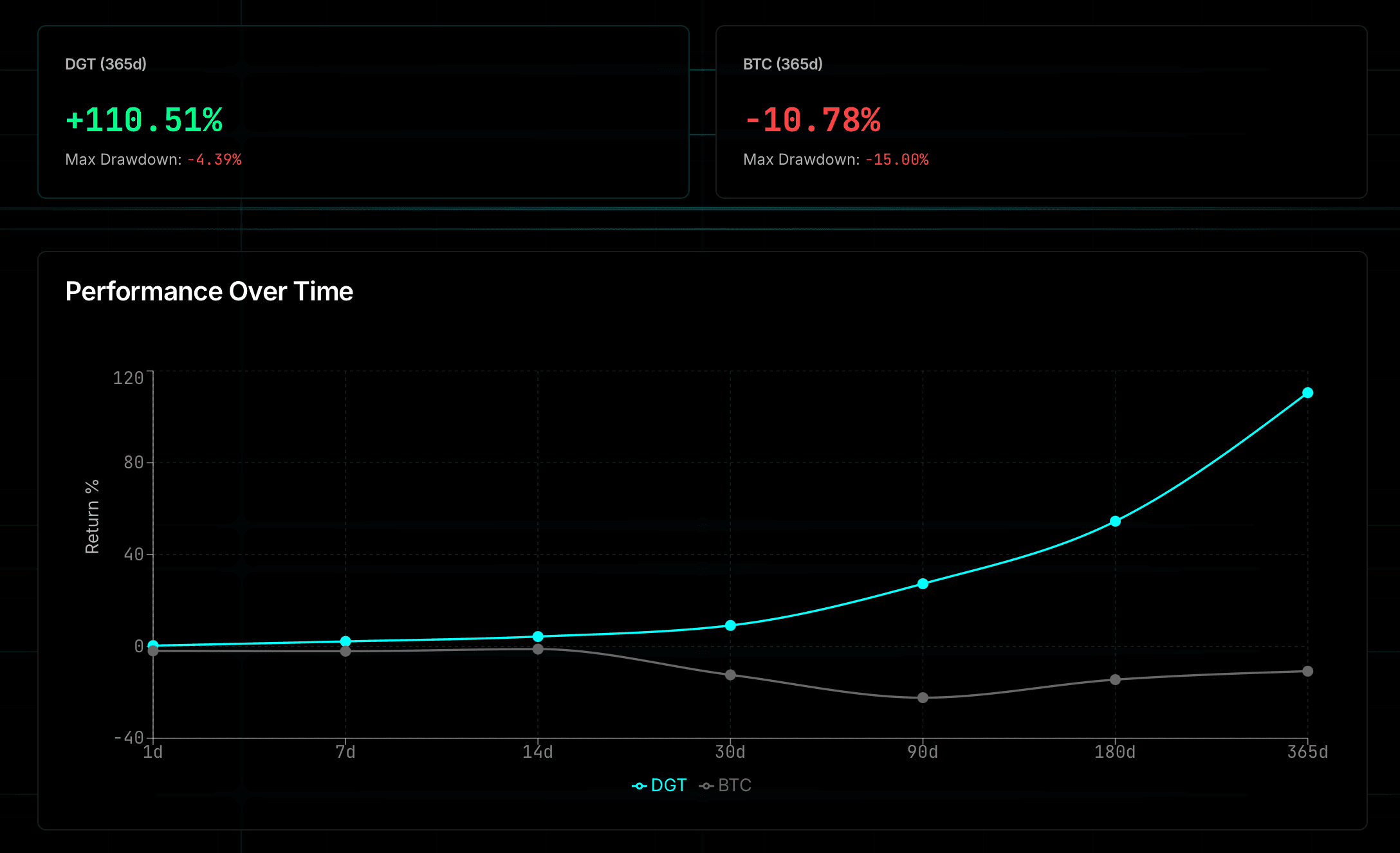

I built GridTrader to democratise sophisticated algorithmic trading strategies and to address a gap I identified in the cryptocurrency trading landscape. Grid trading is a systematic approach that places buy and sell orders at predetermined price intervals, profiting from market volatility without requiring constant monitoring or precise market timing. This strategy excels in ranging markets and provides a disciplined framework for capturing small, consistent gains whilst managing risk through position sizing and automated rebalancing. The platform is engineered for reliability and performance, utilising Python for the trading engine, VectorBT for backtesting and strategy optimisation, and robust API integration with major cryptocurrency exchanges. The system incorporates machine learning components for parameter optimisation and regime detection, ensuring strategies adapt to changing market conditions. Recognising that overfitting is the primary pitfall in quantitative trading, I implemented rigorous validation through Optuna for hyperparameter optimisation combined with walk-forward analysis across multiple time windows. The backtesting framework stress-tests strategies across a wide range of market regimes—including bull markets, bear markets, high volatility periods, and ranging conditions—to ensure robustness beyond historical coincidence. I further employed perturbation testing, introducing controlled noise and parameter variations to validate that profitable patterns represent genuine market inefficiencies rather than artefacts of curve-fitting. This architecture demonstrates the intersection of quantitative finance, software engineering, and practical trading execution. I developed GridTrader after recognising that whilst grid trading is popular amongst experienced traders, existing solutions were either prohibitively expensive or lacked the sophistication necessary for consistent profitability. Having worked as a risk quant in commodities trading, I understood both the mathematical foundations and practical implementation challenges—particularly the danger of strategies that appear excellent in backtests but fail in live markets. The result is a platform I use for my own trading whilst making these institutional-grade strategies accessible to others. I continue to enhance the system with advanced features including multi-timeframe analysis and dynamic grid adjustment.